C'est pas un bien mensuel qu'ils te "vendent"....Videotron, Bell, etc c'est un bien mensuel, alors c'est normal qu'il n'y a pas d'interet. Mais paye un mois en retard, tu verras qu'il y en aura.

C'est la meme chose avec les plaques. C'est un prix pour l'annee...si t'a besoin d'aide pour payer mensuellement au lieu d'une shot pas de trouble ils te le feront, mais ca va couter un extra pcq tu dois etre mis dans le systeme de paiements au mois.

Je vois toujours pas l'arnaque.

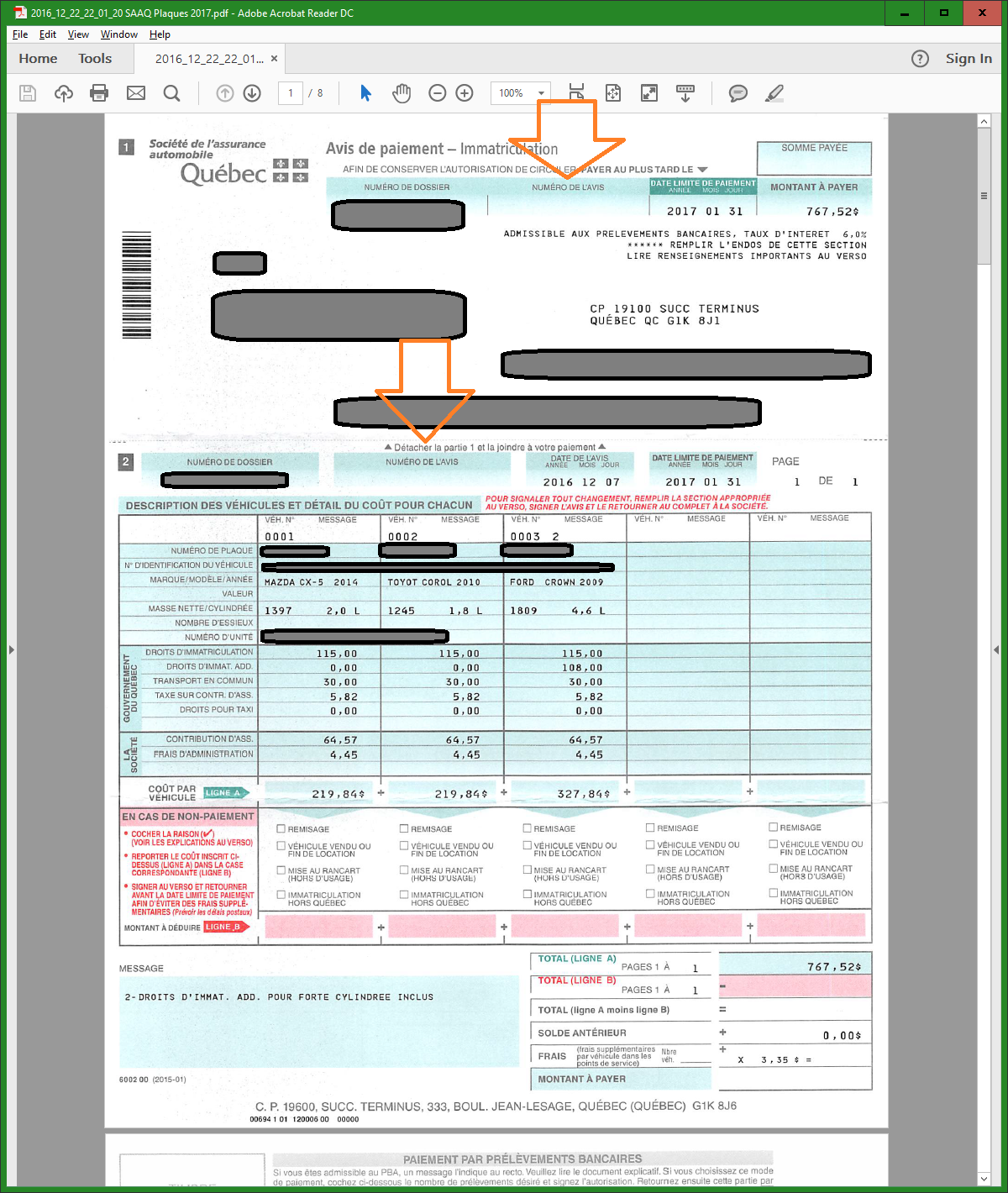

Je regrette, videotron, bell etc c'est des contrats bi-annuels ou annuels. On parle pas de payer en retard non plus, la SAAQ nous charge l'interet avant le temps. Un taux d'interet par definition c'est le montant qu'on paye au creancier pour le risque qu'il prend a financer un enprunteur.

Pour financer de quoi il faut qu'on l'ait. Sinon on appelle ca une mise de cote et c'est ILLEGAL de charger quoi que ce soit pour une mise de cote.

Imagine si tu vas au Hart pour faire mettre de cote ton set de vaisselle et qu'ils te disent "Ok mais ca va te couter 6% de plus que si tu le payes et emportes." Je pense tu arreterais de magasiner chez Hart.

")

LG

have you ever done any finance classes... not the basic ones...

(I'm not questioning your level of intelligence btw, I know you're a smart guy)

Bell/Rogers/Telus (I'm making this as basic as possible) or ANY company (probably the one you work for as well), calculate the average cost of capital/profit/method of payment they receive their $/days receivable

So if you think big businesses set prices and then lose a 2% on credit card out of their pockets, you're wrong.....if you think businesses accept checks and don't calculate the cost of giving a net30/45/60 on their prices, you're wrong

These are ALL calculated with previous years stats, with the upwards/downward trend of each payment method/delays and so on and so forth

the SAAQ can charge 6% interest yearly because they do NOT want everyone to pay using pre-authorized payment and CANNOT charge that to everyone else who won't be using that method because it would be showing in their pricing structure (and would make you 100x angrier)

you think its a scam.... coolio.... but 12$ a year for pre authorized debit from my account... sign me up...and thats exactly it.... I SIGNED UP TO IT... I ACCEPTED THE TERMS AND CONDITIONS OF PAYING 6% YEARLY FOR THAT SERVICE.... if they start giving that to everyone for 0% interest, everyone will jump on that service and after the first year you'll see in the news the finance minister saying the rates for plates and license will slightly go up to compensate the cost of financing everyone

anyways I think just this reply cost me more than the 12$ I pay yearly in interest... back to work...

I agree about the credit card fees. I agree 100000000%,

but the SAAQ does not give you credit. You are simply paying as you go monthly. I still think it's not unreasonable to expect to pay for something as we use it, not "for the future."

I understand if you decide to buy furniture from The Brick and they say fine, use our Brick credit card and you can pay the 2000$ over 24 equal payments + x.x% interest. This is the normal - LEGAL - way of doing things. Has been since the 1950s when diners' club came up with the idea of future earnings and financing.

Especially if you consider that when they reimburse you - like when I put my Sidekick in storage - they don't reimburse you the "pro-rata" rate but they reimburse you only the registration fees which only count for < 40% of the total cost to the consumer.

BTW: Stating that you've accepted the terms does not make them legal. There are many scams where people have accepted terms but then once they realize they've been swindled they go see a court and the contract is cancelled because the terms are illegal or abusive.

Just because we accept this behaviour from the SAAQ does not make it legal.